What Is a Break-Even Analysis?

A breakeven analysis is a calculation that tells business owners the minimum number of units of a good or service they must sell to cover all their costs and to be profitable. It helps entrepreneurs come up with a pricing strategy that will not only cover costs but will generate a gross profit.

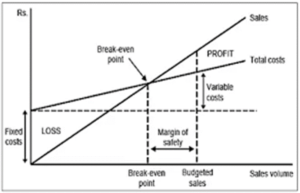

Analyzing different price levels relating to various levels of demand, the break-even analysis determines what level of sales are necessary to cover the company’s total fixed costs.

Types of costs

It’s essential to include all the fixed and variable costs of your business to calculate a break-even point.

Fixed costs

Fixed costs are costs that remain the same regardless of how many units are sold. Rent and insurance could be two examples of fixed costs.

Variable costs

A variable cost is a corporate expense that changes in proportion to how much a company produces or sells. Variable costs increase or decrease depending on a company’s production or sales volume—they rise as production increases and fall as production decreases. (Cost of goods sold)

Contribution Margin (Gross Profit)

The concept of break-even analysis is concerned with the contribution margin of a product. The contribution margin is the excess between the selling price of the product and the total variable costs. For example, if an item sells for R100, the total fixed costs are R25 per unit, and the total variable costs are R60 per unit, the contribution margin of the product is R40 (R100 – R60). This R40 reflects the amount of revenue collected to cover the remaining fixed costs, which are excluded when figuring the contribution margin.

How Break-Even Analysis Works (Break-even point)

The break-even point is the point at which total cost and total revenue are equal, meaning there is no loss or gain for your small business. In other words, a business has reached the point at which its sales exactly cover its expenses.

How to calculate break-even point

To identify your business’s break-even point per product or service, you must identify all your costs—for both operating your business and making your product. Here’s the formula for a break-even analysis that calculates how many products you need to sell to break even:

Break-even point in quantity of units sold = Fixed costs/(Price per unit – Variable cost per unit)

Pricing a product, the costs incurred in a business, and sales volume are interrelated.

In general, a company with lower fixed costs will have a lower break-even point of sale. For example, a company with R0 of fixed costs will automatically have broken even upon the sale of the first product assuming variable costs do not exceed sales revenue.

Calculations for Break-Even Analysis

The calculation of break-even analysis may use different calculations. But we will just look at one calculation. In this calculation, we will divide the total fixed costs by the unit contribution margin. In the example above, assume the value of the entire fixed costs is R20,000. With a contribution margin of R40, the break-even point is 500 units (R20,000 divided by R40). Upon the sale of 500 units, the payment of all fixed costs are complete, and the company will report a net profit or loss of R0.

Why is break-even analysis important for businesses?

Cost calculation

A break-even analysis can help you to determine whether your business will remain profitable if you increase your company’s fixed costs—if you choose to move to a bigger and more expensive office space, for instance, or hire another salaried employee.

Budgeting and setting targets

A break-even analysis can help you budget by providing an estimate of your profitability in an upcoming month, quarter, or year.

Motivational tool

A break-even analysis can help you to set sales benchmarks and, hence, motivate you to work harder when you know the profitability of your business is at stake.

Margin of safety

In break-even analysis, the term margin of safety indicates the amount of sales that are above the break-even point. In other words, the margin of safety indicates the amount by which a company’s sales could decrease before the company will have no profit.

Example of Margin of Safety

Let’s assume that a company currently sells 3,000 units of its only product. The company has estimated that its break-even point is 2,800 units. Therefore, the company’s margin of safety is 200 units.

You can calculate the margin of safety by deducting the breakeven point from the current or estimated sales.

Tips for lowering your break-even point

If the results of your initial break-even analysis aren’t what you had hoped for, let’s look at how you can change your current plan to reach a break-even point that works for your business.

Reduce fixed costs

If your business has a high number of fixed costs, it can create a lot of pressure on expenses with sales revenue. The more you can reduce fixed costs, the less revenue your business will need to earn to break even. For example, you may need to rent a smaller place.

Reduce variable costs

Variable costs, such as manufacturing or shipping, fluctuate based on your sales volume. To reduce your variable costs, you might consider negotiating a lower cost by offering to purchase a minimum quantity every month.

Increase your selling price

If you’re unable to break even based on the current price of your product or service, you may need to increase that price. By raising your price, you reduce how much you need to sell in order to break even.

When evaluating this option, it’s important to consider what your customers are willing to pay and how their expectations may change if your product or service goes up in price. For example, your customers may expect a higher-quality product or more responsive customer service- Consider elasticity of demand. The elasticity of demand refers to the degree to which demand responds to a change in an economic factor, say change in price.

In some cases, your sales volume may decline as your prices go up, but as long as the increase in price is greater than the dip in sales volume, it may still be the right option for your business.

Improve your sales mix

Rather than raising prices across the board, if your business sells multiple products or services, you could focus on increasing the sales of products and services with high contribution margins.

Conclusion

A break-even analysis is a simple tool for entrepreneurs to estimate their business’s profitability. By understanding the variables impacting your break-even point, you can better evaluate elements of your pricing model that may need adjusting to give your business the best possible chance to earn a profit.

Break-even analysis tells you how many units of a product must be sold to cover the fixed and variable costs of production.

The break-even point is considered a measure of the margin of safety.

It is also a powerful tool for planning and decision making, and for highlighting critical information like costs, quantities sold, prices, and so much more.